6th February 2026, Gaurav Kumar Singh

A few years ago, investing in the National Pension System felt like setting money aside in a locked cupboard. You knew it was safe. You knew it was meant for retirement. But accessing it, adjusting it, or tailoring it to your life stage was—let’s be honest—frustrating.

Fast forward to today, and the cupboard finally has shelves, drawers, and keys you can actually use.

The new NPS rules have officially been adopted, marking one of the biggest overhauls in the system’s history. These changes fundamentally alter how you invest, how much risk you can take, and how easily you can withdraw your money—both before and after retirement.

Let’s break it down in the simplest way possible: what the old rules were, what the new rules are, and why the difference matters to you.

Why NPS Needed a Change?

Under the old NPS framework, discipline was the top priority. Flexibility came second. The system assumed that every investor had a stable career, predictable income, and a similar retirement path.

But real life doesn’t work like that anymore.

People switch careers, take breaks, start businesses, and work well beyond traditional retirement ages. The old rules began to feel restrictive—especially when compared to other long-term investment options.

The new NPS rules aim to fix that imbalance.

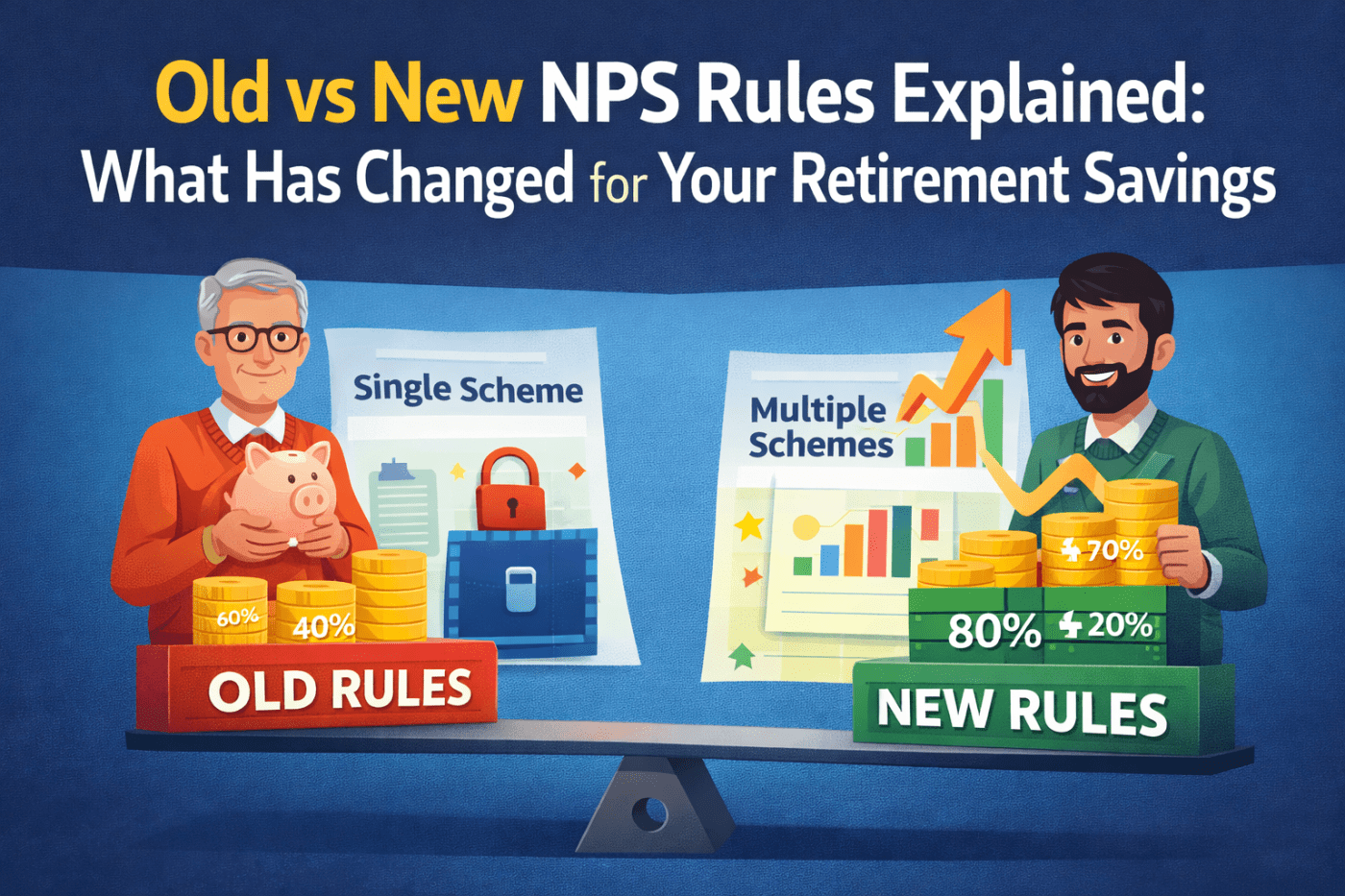

Single Scheme vs Multiple Scheme Framework

Under the old NPS rules, a subscriber could hold only one scheme per asset class within a single Permanent Retirement Account Number (PRAN). Even if your income grew or your risk appetite changed, you were largely stuck with the same structure.

Under the new NPS rules, this limitation is gone.

You can now invest in multiple schemes under a single account through the Multiple Scheme Framework. Each scheme can have its own asset mix, risk profile, and investment objective.

Think of it like upgrading from a single savings jar to a full financial toolbox. One scheme can focus on aggressive growth during your early career, while another gradually shifts to stability as retirement approaches.

Equity Allocation: From Conservative to Customizable

Earlier, equity exposure in NPS was capped at 75%, regardless of how young or aggressive an investor you were. This cap often limited long-term wealth creation, especially for subscribers in their 20s and 30s.

Under the new NPS rules, pension fund managers can now offer schemes with up to 100% equity exposure.

This doesn’t mean everyone should rush into equities. But it gives younger investors the option to align their NPS investments with long-term growth potential, similar to how equity mutual funds are used for wealth creation.

In short, the old rules protected investors from volatility. The new rules empower them to manage it.

Exit Rules: Old Rigidity vs New Flexibility

Early exit was one of the biggest pain points in the old NPS system.

Previously, even after completing the required tenure, 80% of the corpus had to be used to buy an annuity, leaving only 20% as lump sum. This applied regardless of personal financial needs.

Under the new rules, this has changed significantly.

If you exit before retirement after meeting the minimum vesting period, only 40% must be annuitised, while 60% can be withdrawn as lump sum. This provides much-needed liquidity during mid-life transitions such as career changes, medical needs, or entrepreneurial ventures.

Retirement Withdrawal: A Major Shift

At normal retirement age, the difference between old and new rules is striking.

Under the old rules, you could withdraw 60% as lump sum, while 40% was mandatorily annuitised.

Under the new NPS rules, this flips in your favour. You can now withdraw 80% as lump sum, and only 20% needs to be used for annuity purchase.

For retirees, this is a big win. It allows greater control over retirement income planning, especially in an environment where annuity returns are often modest.

However, it also places greater responsibility on retirees to manage their funds wisely.

Taxation: What Stayed the Same (and What Didn’t)

While withdrawal flexibility has increased, tax rules remain an important consideration.

Even under the new system:

Only 60% of the total corpus withdrawn remains tax-free The remaining lump sum is taxed according to income tax slabs

So while you can withdraw more, careful tax planning is essential to avoid unpleasant surprises.

Relief for Small Corpus Holders

Under the old rules, full lump-sum withdrawal was allowed only if the total corpus was ₹5 lakh or less.

Under the new rules, this threshold has increased to ₹12 lakh, with ₹6 lakh completely tax-free.

This change recognises that mandatory annuitisation makes little sense for small retirement savings and provides meaningful relief to low and middle-income subscribers.

Premature and Partial Withdrawals: Then vs Now

Earlier, premature withdrawal was capped at ₹2.5 lakh, and partial withdrawals were limited in number and purpose.

Under the new NPS rules:

Premature withdrawal limit increases to ₹4 lakh Partial withdrawals can be made up to six times, instead of three. Withdrawal amounts are calculated based on the corpus available at the time

For a long-term product, this added flexibility makes NPS far more practical.

Joining and Continuation Age: Reflecting Modern Careers

Under the old rules, continuation was limited and not well-suited for those working longer.

The new framework allows:

Entry up to 70 years Continuation up to 85 years

This aligns NPS with modern career patterns where retirement is increasingly gradual rather than sudden.

Loan Against NPS: A New Feature

Earlier, loans against NPS were not permitted at all.

The new rules allow loans against the NPS corpus, reducing the need for premature withdrawals and making NPS more comparable to other long-term savings instruments.

The Bigger Picture: Freedom with Responsibility

The old NPS rules emphasised discipline above all else.

The new NPS rules prioritise choice, flexibility, and personalisation.

This transformation makes NPS more powerful—but also demands better financial awareness from investors. With greater control comes the need for thoughtful planning, especially around risk, taxation, and retirement income strategies.

Final Thoughts: A Modern NPS for a Modern India

The shift from old to new NPS rules marks a turning point in India’s retirement landscape. What was once a rigid pension product is now a flexible, customizable retirement platform.

If you are already an NPS subscriber, this is the right time to reassess your investment strategy. If you were hesitant earlier, the new rules may finally make NPS relevant for you.

Retirement planning isn’t about locking money away—it’s about preparing for life as it unfolds.

How do you feel about the new NPS rules compared to the old ones? Share your thoughts, start the conversation, and explore how to make your retirement truly future-ready.

If you found this article valuable, please don’t forget to Like and Subscribe to my blog for more expert insights and updates.

Leave a comment