11th May 2025, Gaurav Kumar Singh

“I’ll just pay the minimum this month and clear the rest later.”

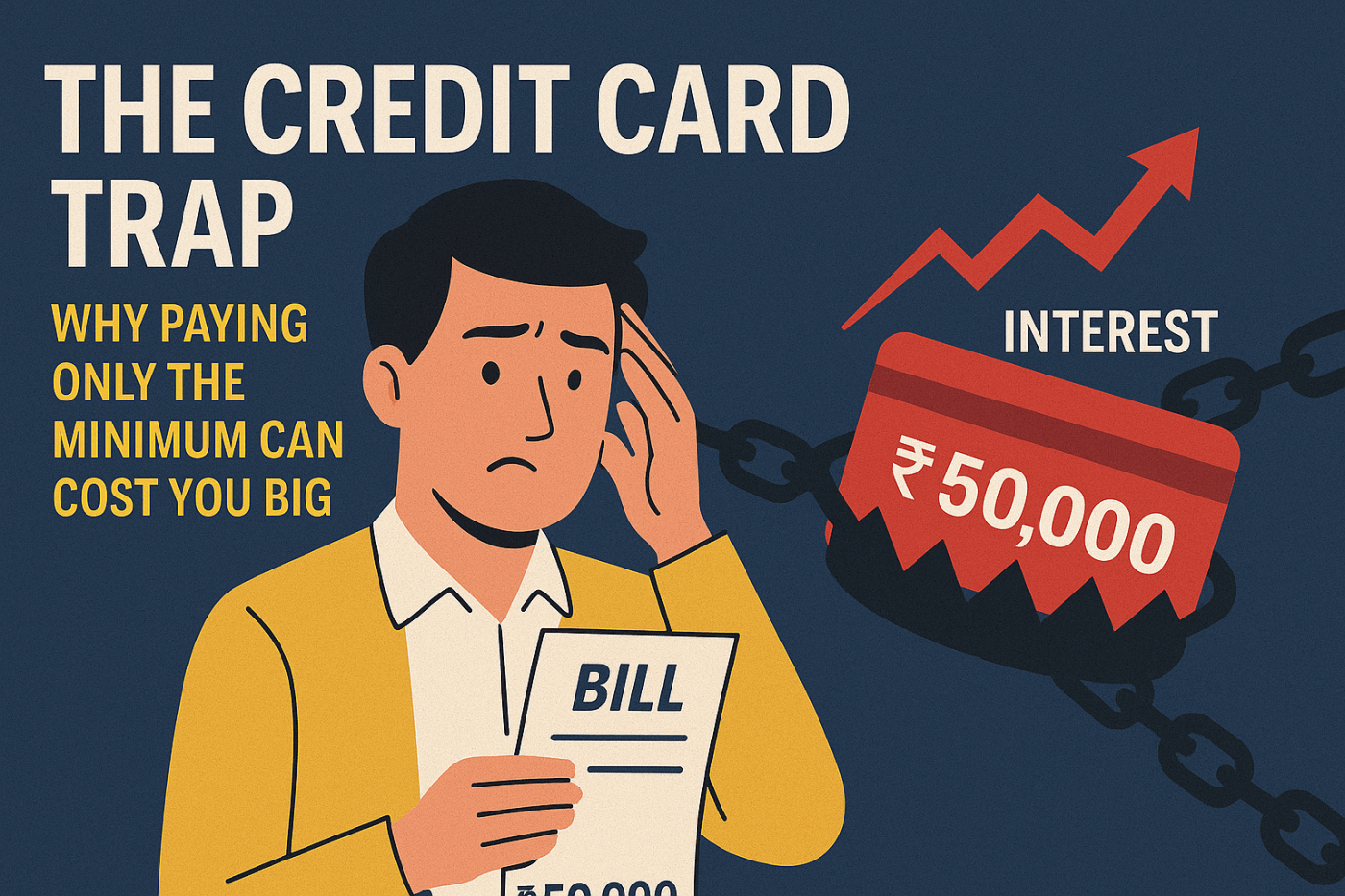

If you’ve ever said this to yourself after looking at your credit card bill, you’re not alone—but you might be setting yourself up for a long, expensive debt trap.

In this article, I’ll break down why paying only the minimum balance on your credit card is a dangerous habit, how it affects your finances in the long run, and what you should do instead.

The Illusion of Minimum Payment: A Real-Life Example

Let’s say you have a credit card outstanding balance of ₹50,000. Your card issuer charges an Annual Percentage Rate (APR) of 20%, which translates to a monthly interest rate of 1.67%. Sounds manageable, right?

Now, here’s the catch: your minimum payment is just 2% of the outstanding amount—that’s ₹1,000 for the first month.

Here’s what really happens when you only pay the minimum every month:

The Breakdown (Over 12 Months):

Total paid in 12 months: ₹11,815.31

Total principal reduced: ₹1,808.93

Remaining balance after a year: ₹48,191.07

Wait, what?

You paid over ₹11,800, and your debt only reduced by ₹1,800? Where did the rest of the money go?

Answer: Interest.

Every month, your interest eats up most of your payment. For example:

Month 1:

You pay ₹1,000 Interest: ₹835

Principal paid: Only ₹165

This pattern continues, and the balance barely goes down.

Why This Is Dangerous

This is called the Minimum Payment Trap. It’s a cycle where:

You keep paying the minimum.

Your outstanding barely reduces.

You continue to get charged interest on a high amount.

You’re stuck in debt for years—even without spending a rupee more.

Now imagine if you continue to use your card while making only minimum payments. Your balance can grow faster than you can pay it off.

Real-World Impact: The True Cost of Convenience

Let’s compare two scenarios:

1. Minimum Payment Strategy

Balance: ₹50,000

Total Paid in 1 Year: ₹11,815

Balance after 1 Year: ₹48,191

Total Interest Paid: ₹10,000+

Debt-free timeline: Over 5 years, possibly more (if you stop spending)

2. Aggressive Repayment Strategy

Let’s say you commit to paying ₹5,000/month:

You’ll clear the debt in roughly 11 months

Interest paid: Just around ₹4,500

You save time and ₹6,000–₹8,000 in interest

Better Alternatives to Escape the Trap

Here’s how you can avoid or escape the minimum payment trap:

1. Always Pay More Than the Minimum

Try to pay off the entire balance or at least as much as you can. Every extra rupee goes directly toward reducing your principal.

2. Use the Avalanche or Snowball Method

Avalanche Method: Pay off the card with the highest interest rate first. Snowball Method: Pay off the smallest debt first for a motivational boost.

3. Consider a Balance Transfer

If your credit score is good, consider transferring your balance to a low or 0% interest card for a limited period. This can save you thousands in interest.

4. Create a Debt Payoff Plan

Make a budget, cut unnecessary expenses, and commit to clearing your debt in a fixed time frame.

Conclusion: Don’t Let Convenience Cost You

Credit cards offer flexibility, rewards, and convenience—but only if used wisely. Paying just the minimum might seem like an easy way out, but it’s actually a financial trap that benefits only the bank, not you.

Take control of your credit card payments, pay more than the minimum, and protect your future finances.

Because the longer you stay in debt, the more it costs you—not just in money, but in peace of mind.

Liked this blog?

Share it with someone who needs to hear this.

Subscribe to the Blog for more personal finance tips, smart money habits, and debt-free living strategies.

If you found this article valuable, please don’t forget to Like and Subscribe to my blog for more expert insights and updates.